When you read the news, you often see headlines like, "The national average mortgage rate dropped to 6.5% today." But when you actually call a lender to get pre-approved, you might be quoted 6.8%, 7.2%, or even 6.1%. Why is there such a massive difference between the news and your reality?

The truth is that the "national average" is just a baseline. The actual interest rate you are offered is calculated using a highly specific, standardized formula. Let's pull back the curtain and look at the exact rules lenders use to calculate your mortgage rate.

1. The 70% Rule: Fannie Mae and the LLPA Matrix

Approximately 70% of all mortgages in the United States are "Conventional Loans." These are loans that banks issue to you, but then immediately sell to government-sponsored enterprises like Fannie Mae or Freddie Mac.

Because Fannie Mae buys these loans, they dictate the pricing rules. They use a system called Loan-Level Price Adjustments (LLPA). This is essentially a giant grid (a matrix) that maps your Credit Score (FICO) against your Down Payment (LTV - Loan-to-Value).

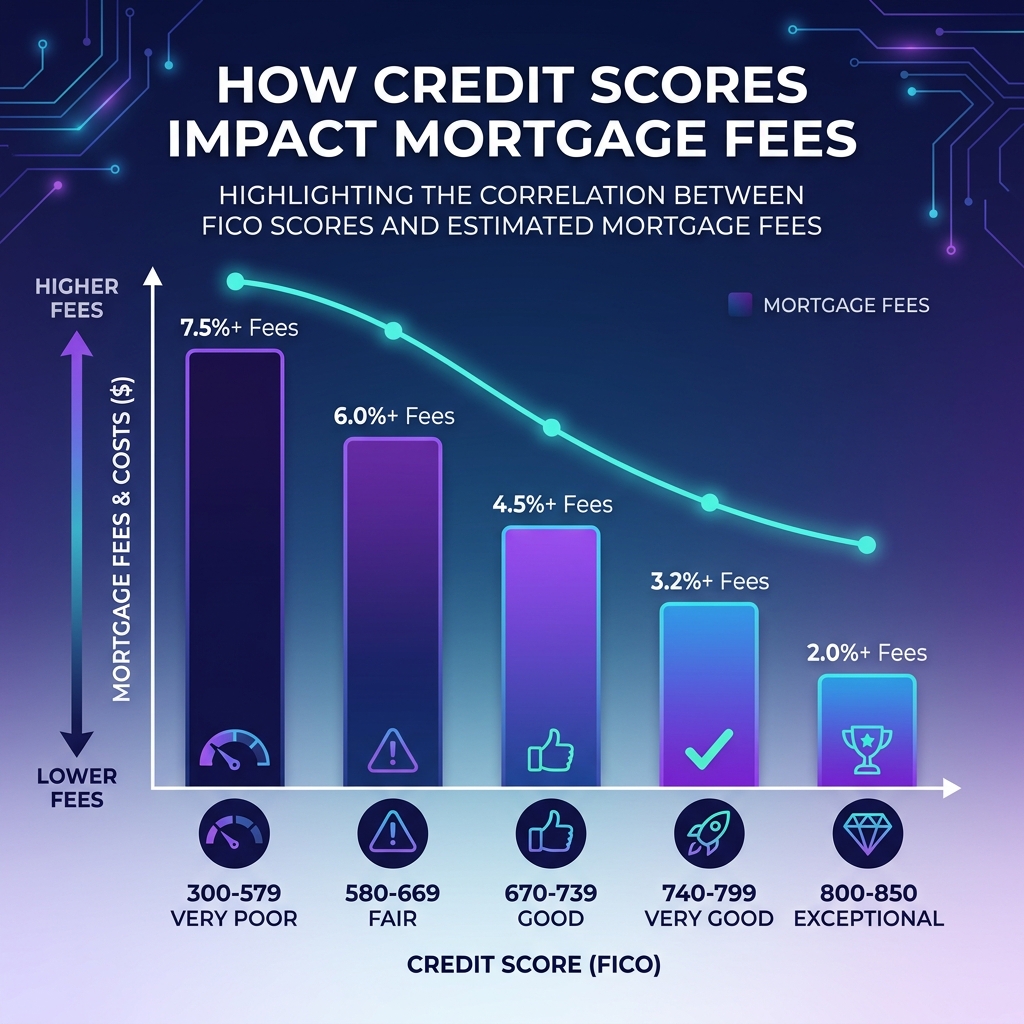

Lower credit scores result in significantly higher upfront fees, which lenders convert into higher interest rates.

According to the official Fannie Mae LLPA Matrix (which was last significantly updated in 2023 by the FHFA), lenders must charge you an upfront fee based on your risk profile. For example, if you are buying a house with 20% down:

- A borrower with an 780+ credit score pays a 0.375% fee.

- A borrower with a 680 credit score pays a 1.500% fee.

- A borrower with a 640 credit score pays a 2.250% fee.

2. How "Fees" Become "Interest Rates"

You might be wondering: "If LLPA is an upfront fee, why does my interest rate change?"

Most homebuyers do not want to bring an extra $5,000 to $10,000 in cash to the closing table just to pay these Fannie Mae fees. To solve this, banks "absorb" the upfront fee for you, and in exchange, they raise your interest rate. This is known in the industry as Discount Points.

According to both the Consumer Financial Protection Bureau (CFPB) and major banks, there is an industry-standard conversion rule:

The Rule of Thumb: Every 1.00% of upfront fee equates to approximately a 0.25% increase in your annual interest rate (APR).

So, if the LLPA matrix says a 640 credit score has a fee that is ~1.875% higher than a 780 credit score, the bank will increase the 640 borrower's interest rate by approximately 0.47%.

We have pre-calculated the LLPA spread for every FICO tier. Find your exact credit score here to see what interest rate you can expect today.

3. What About the Other 30% of Mortgages?

If Fannie Mae controls 70% of the market, what happens to the rest? The remaining 30% are non-conventional loans, and they completely ignore the Fannie Mae LLPA matrix.

Government-Backed Loans (FHA & VA)

Insured by the government (Ginnie Mae), these loans are highly forgiving. For instance, an FHA loan allows credit scores down to 580 and does not impose massive LLPA interest rate penalties. In fact, a borrower with a 620 score will often get a lower base interest rate on an FHA loan than a conventional loan. However, the government charges hefty Mortgage Insurance Premiums (MIP) to balance the risk.

Jumbo Loans and Non-QM

If you are buying a multi-million dollar property that exceeds federal loan limits, or if you are self-employed using bank-statement loans (Non-QM), Fannie Mae will not buy your loan. The bank holds the loan on its own books. Therefore, private banks set their own strict risk models, usually requiring massive down payments and 700+ credit scores.

Summary

Your mortgage rate isn't randomly pulled from the news. It is a highly mathematical calculation based primarily on your FICO score and your down payment. By improving your credit score even by 20 points, you can bump yourself into a better LLPA tier and save thousands of dollars over the life of your loan.