One of the most common questions prospective buyers ask in 2026 is, "Is now a good time to buy a house, or should I wait for prices and rates to drop?" It is a natural concern, as a home is likely the largest financial purchase you will ever make.

However, the truth about the housing market is that trying to perfectly time the market is nearly impossible. Instead of focusing entirely on macroeconomic trends, the better question to ask is: "Is now a good time for ME to buy a house?"

What the Experts Predict for 2026

According to major real estate and financial authorities, the 2026 housing market is characterized by modest growth and stabilization, not a dramatic crash. Here are the key forecasts from independent sources:

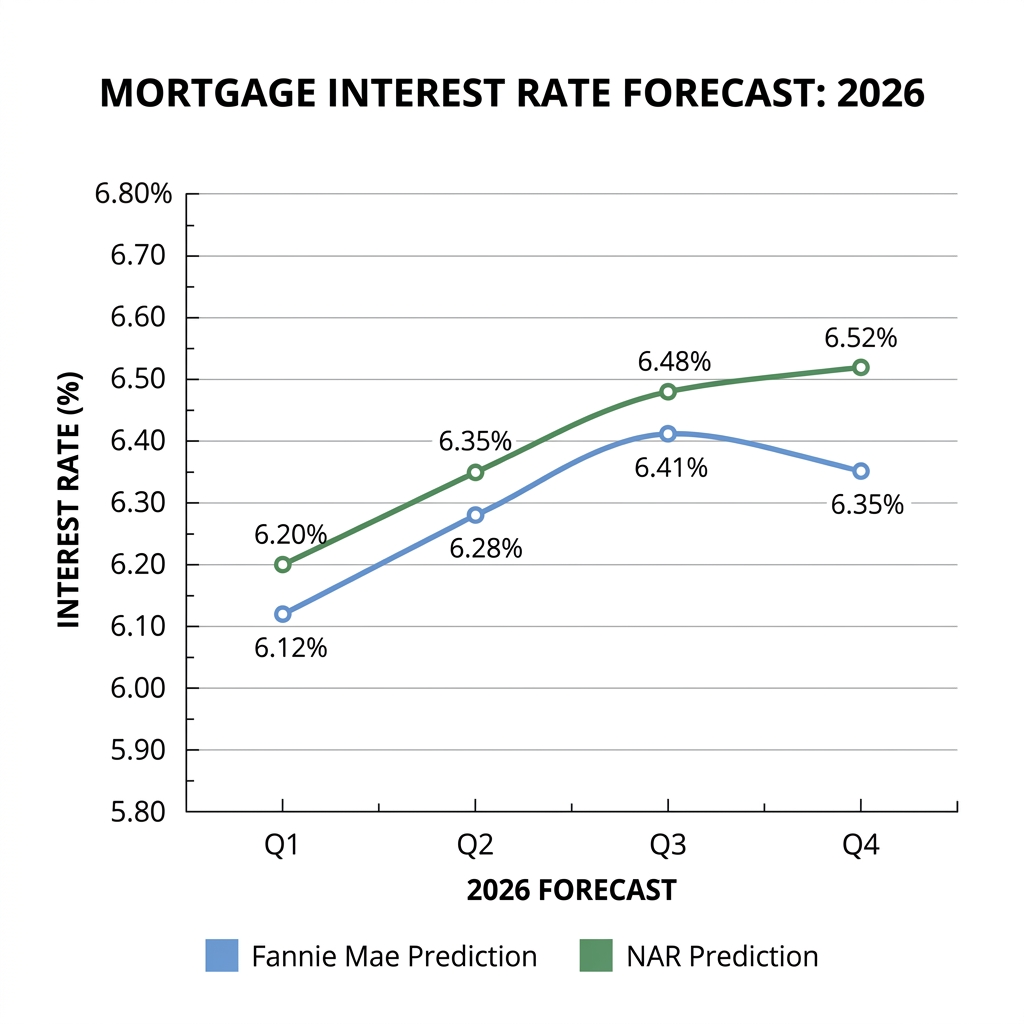

- National Association of Realtors (NAR): NAR projects that both existing-home sales and median home prices will rise by approximately 4% in 2026. They also anticipate mortgage rates to average around 6.5%. Source: NAR

- Fannie Mae: Fannie Mae’s economic forecast expects 30-year fixed mortgage rates to hover in the 6.1% to 6.3% range through late 2026. They project home price growth of roughly 3.2% due to limited inventory. Source: Fannie Mae

The Danger of "Timing the Market"

Many buyers sit on the sidelines waiting for either home prices to crash or interest rates to plummet. But historical data from the Federal Reserve (FRED) shows that these two factors often work like a seesaw:

- When interest rates drop significantly, buyer demand floods the market. This increased competition drives home prices up and often leads to bidding wars.

- When interest rates rise, buyer demand cools, and home prices tend to stabilize or soften.

If you wait for the "perfect" combination of low prices and low rates, you may end up waiting indefinitely while continuing to pay rent and missing out on building equity.

Focus on Personal Financial Readiness

The best time to buy a house is when you are personally and financially ready. You should strongly consider buying if you meet the following criteria:

- You have a stable income: You feel secure in your job and expect your income to remain stable or grow.

- Your debt is manageable: Your Debt-to-Income (DTI) ratio is low enough that adding a mortgage payment won't cause financial stress.

- You have savings: You have enough saved for a down payment, closing costs, and an emergency fund to cover unexpected home repairs.

- You plan to stay: You plan to live in the home for at least 5 to 7 years. Buying for a shorter term is risky because closing costs can wipe out any short-term appreciation.

Not sure if your budget can handle a house right now? Use our Affordability Calculator to see exactly how much house you can safely buy without becoming "house poor."

The Final Verdict

If you find a home you love, you can comfortably afford the monthly payments including taxes and insurance, and you plan to stay in the area for a long time, then yes—now is a good time to buy. If interest rates eventually drop in the future, you always have the option to refinance to a lower rate later.